Lauren Williams here, and instead of preparing our typical market update reviewing last month’s data, I felt it would be a good time to address the current market volatility.

Although as of the publication of this report, the markets have regained much of early March’s losses, there’s no denying that investors have been through a whirlwind over the past several weeks. Markets are doing what they sometimes do, which is perform erratically, and headlines are filled with talk of tariffs, government spending debates, and broader economic uncertainty.

If you’re feeling uneasy right now, you’re not alone.

But moments like these are an important time to pause, take a breath, and step back for some perspective on what’s really going on — and remember that this isn’t the first time markets have been rocked by policy moves.

First, let’s talk about what’s driving this wave of market volatility.

Much of the turbulence is tied to growing uncertainty around trade and tariffs. The constant back-and-forth over potential tariffs, especially with countries like China, Mexico, and Canada, has left businesses and investors confused about what’s coming next. That confusion is causing markets to bounce up and down, sometimes dramatically within a single day. On top of that, government spending decisions and shifting political priorities are making it difficult for companies to plan ahead, adding yet another layer of uncertainty. Even though it might feel like markets are in freefall, it’s worth noting that overall declines in the major indexes haven’t been nearly as steep as they feel when you’re watching the headlines.

But here’s what’s important to remember: we’ve been here before. Remember this famous hawkish line?

“While higher interest rates, slower growth, and softer labor market conditions will bring down inflation, they will also bring some pain to households and businesses. These are the unfortunate costs of reducing inflation. But a failure to restore price stability would mean far greater pain.” – Jerome Powell

When the Federal Reserve wanted to put a stop to excess spending to rein in inflation in August of 2022, Fed Chair Jerome Powell stood up in front of the world and essentially said, “This is going to hurt.” And it did. Markets continued their tumbled into November 2022 as investors came to terms with the reality of rising rates, tighter monetary policy, and an end to easy money. But that period of “necessary pain” set the stage for cooling inflation and a healthier economy.

Fast forward to today, and we are seeing a similarly aggressive, hawkish stance—this time on trade and fiscal policy. The current administration has made it clear that tariffs and aggressive trade policies will remain a central part of its agenda. These moves are not just about trade; they ripple into tax policy, immigration, and global security — creating layers of uncertainty that markets are struggling to price in. Just like Powell in 2022, the president has signaled his willingness to “trample markets” temporarily to achieve longer-term goals. What we are seeing now is not unprecedented — it’s another chapter in how bold policy shifts can jolt markets.

Over the weekend, the president notably acknowledged that he wouldn’t rule out a recession—a comment that clearly rattled markets. While that statement may be unsettling for investors in the short term, there are strategic political reasons why a recession could actually help advance certain policy goals.

What could be gained from a recession?

First, it would create a powerful opportunity to push for lower taxes and exert pressure on the Federal Reserve to cut interest rates. The current administration has already been floating ideas for the new tax package, and if the economy begins to weaken, they could easily argue, “See? Now we need to cut taxes to stimulate growth.” A downturn would give them both the justification and the political momentum to pursue aggressive fiscal and monetary policies that might be much harder to pass during periods of steady growth.

In fact, while recessions are generally feared for the pain they bring to households and businesses, they can also create a pathway to achieve three major policy objectives: tax cuts, lower interest rates, and reduced prices. Here’s how:

- Tax Cuts: Recessions create political pressure for stimulus measures, and tax cuts are often a favored tool to encourage economic recovery. The administration could argue that reducing taxes—especially corporate and income taxes—would help businesses and consumers regain footing, making it an easier sell politically.

- Lower Interest Rates: The Federal Reserve typically lowers interest rates during a recession to stimulate borrowing and investment. If a downturn were to occur, the Fed may feel compelled to cut rates more aggressively, which could benefit certain industries and real estate markets.

- Price Reduction: A recession typically weakens demand, leading businesses to lower prices to attract cautious consumers. This could help curb inflation, something the current administration may see as a necessary adjustment after years of elevated prices.

So, where does the economy stand? The reality is a bit complicated — but far from catastrophic.

As of February 28th, 2025, most of our leading economic indicators pointed towards healthy expansion.

Yes, there are areas slowing down, particularly in consumer and business spending. But much of that slowdown is a result of unusual activity late last year. Many companies and households rushed to buy goods — appliances, cars, industrial supplies — in anticipation of tariffs that hadn’t yet taken effect. That burst of activity made the economy look unusually strong at the end of 2024. Now, as that demand has been “pulled forward,” spending appears to be softening. Think of it like everyone in town buying a washing machine in December — naturally, they’re not going to buy another one in March.

While current data may be softening, it doesn’t mean the economy is falling apart.

The job market is also still holding up well, despite some early warning signs. Unemployment remains low at about 4.1%, and companies are still hiring. Yes, some government-related layoffs are beginning to surface, and some surveys, like the Challenger Job Cuts report, have flagged the highest level of announced layoffs since 2020. But so far, there is no broad evidence of a widespread labor market downturn, in fact the US economy added 151,000 jobs last month, according to CNN Business. Private investment, especially in areas like technology, AI, and energy, is still happening — though many businesses are understandably being more cautious because of policy uncertainty. However, it sounds like the steel industry, automotive makers, and chip manufacturers may be on the verge of needing many more employees to fill roles in their new US based manufacturing plants.

Tariffs and the resurgence of inflation are the major sources of uncertainty today.

While tariffs are often framed as a way to protect American companies, the truth is they tend to raise prices on everyday goods — everything from groceries to gas to building materials. And when prices rise, people and businesses spend less, which slows the broader economy and hurts company profits. That, in turn, weighs on stock prices. Even worse, when companies don’t know what policies will be implemented, they often pause hiring and investment decisions, which further slows growth. And right now, many tariffs haven’t even been formally enacted — yet the mere possibility is enough to shake markets and investor confidence.

So, with all this swirling around, what should long-term investors do? The first and most important answer is simple: Don’t make emotional decisions.

It’s important to recognize that what we’re seeing is not broad-based panic-selling — it’s largely strategic positioning. Long-term investors are not “capitulating” — meaning they are not indiscriminately dumping portfolios. Much of the volatility we’re seeing is being driven by institutions and hedge funds taking short-term positions against the market, aiming to profit from fear-based selling. In fact, over the past two weeks, there’s been a notable surge in speculative, short-term trading as opportunistic investors try to capitalize on market jitters. This is tactical maneuvering, not an investor stampede. It’s also not an investment strategy that can be held long-term since markets are typically on the rise 80% of the time.

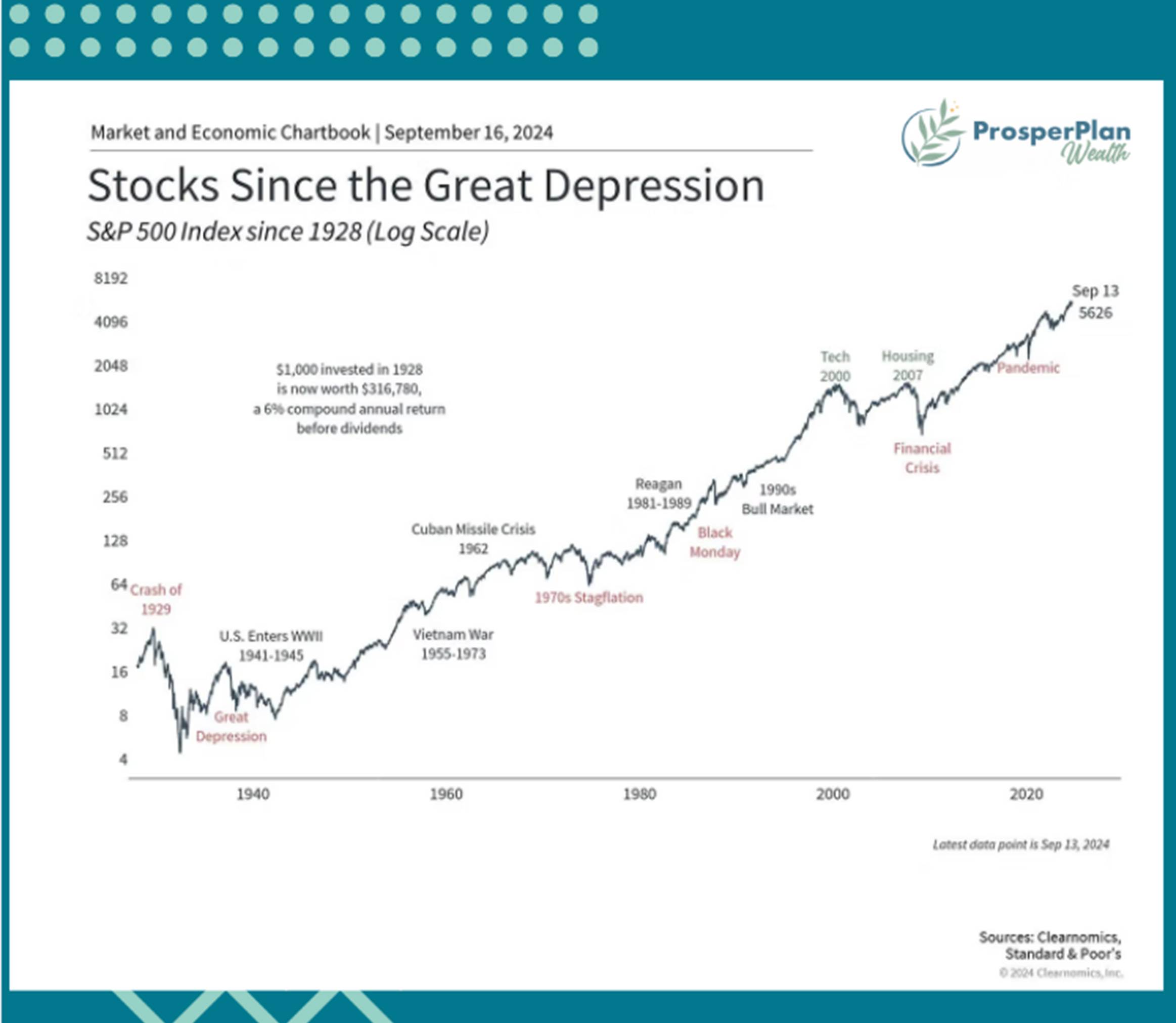

Historically, markets experience pullbacks of 5-10% regularly— even during strong economic expansions. In fact, since World War II, the average market correction of around 10% tends to last about 3 to 4 months before stabilizing or recovering. This is part of the natural rhythm of markets, not a sign that something is fundamentally broken.

However, we’ve also experienced larger events with more severe consequences. Within the last five years, we’ve experienced two downward markets that gave us 20% losses over relatively short periods of time. The average time for recovery following a deeper bear market is about 15-17 months. That being said, historically, we’ve recovered and celebrated new highs after each expected or unexpected market trauma.

History consistently shows that staying invested during periods of volatility leads to stronger long-term outcomes. Some of the market’s best days tend to follow its worst ones, and missing even a few of those rebounds can significantly reduce long-term returns. Trying to time the market rarely works. Selling in a panic often means locking in losses and sitting on the sidelines while the recovery takes shape. As we saw in 2020 and 2023/2024, recoveries can happen quickly, with company valuations swiftly retracing lost ground. Waiting for the “right time” to re-enter the market can often mean missing the rebound entirely.

This is why we remain focused on high-quality companies—businesses with strong balance sheets and resilient earnings—rather than making emotional, short-term moves into cash or defensive assets that may underperform when markets stabilize. Historically, selling during market corrections has been one of the most consistent ways to lose money to more patient and disciplined investors.

For those comfortable with some level of risk, this environment may even present opportunities. Interest rates have begun to ease, and sectors like homebuilders and lenders—both of which struggled under higher rates—could benefit if rates stabilize and economic conditions remain steady. Naturally, the market is closely watching tariff developments, particularly on key materials like lumber and steel, which could impact these industries. But this is exactly why diversification remains critical. A well-structured portfolio is designed to weather all types of market conditions—whether it’s a rapid rebound, extended volatility, or a slower economic cycle.

Most importantly, you’re already ahead of the game. You have a dynamic investment management team on your side, one that is actively assessing opportunities, managing risk, and positioning portfolios with a strategic, disciplined approach. With professional oversight, real-time market insights, and a commitment to long-term success, you have the advantage of an investment strategy that is informed, proactive, and built to navigate uncertain times.

It’s also important to address what’s happening with interest rates and the Federal Reserve. Markets are starting to price in a possible Fed rate cut by June 2025. While that might sound like good news, it would likely only happen if the economy showed signs of deeper weakness. The next set of rate cuts will likely come as a result of economic weakness. That’s why we continue to hold high-quality bonds in portfolios as a stable anchor, and like the Fed, we’re ready to adjust positioning as needed depending on how the economic and market data evolves.

In sum, this is not a time to give up on the market or your long-term plan.

Volatility is part of the natural cycle of investing, even though it rarely feels comfortable in the moment. We expect markets to remain choppy in the near term, but we are navigating this period with steady hands and a focus on long-term outcomes.

If you’re feeling uneasy or wondering how his environment affects your personal plan, we’re always available to have that conversation. Together, we can ensure that your plan accounts for both the expected and the unexpected — and that you remain on track to meet your goals. The market will eventually stabilize. And when it does, those who stayed disciplined and focused on the long term are the ones who benefit the most.

You’ve got this. We’ve got this. Together.

Warm regards,