In response to our last newsletter, a long-time client wrote to me with an entertaining version of a serious question (and one that I think may be on your mind): “With tariffs rising, talk of a possible recession, and the stock market behaving like it skipped its morning coffee—what exactly is your investment management team doing differently to protect my portfolio?”

It’s a reasonable question, especially in times like these. This client had managed her own investments through the 2008 crash, and so she definitely understands what it means to navigate economic uncertainty. And while no two downturns are identical, the concern is valid—especially when last month the media was comparing this to the stagflation of the 1970s, 2008’s long, slow boomerang, and even the Great Depression of nearly a century ago.

Our team at ProsperPlan takes your questions very seriously, and so I thought that right now would be the perfect time to pull back the curtain and share, not just what we’re doing to protect you, but why.

Good? Bad? The Current Environment is Actually a Mixed Bag

Let’s start with the basics, which means the hard economic data. Despite the news cycle’s best effort to give us whiplash, if you look at it dispassionately, the key numbers have actually been surprisingly steady.

- As widely reported in outlets such as Forbes, in April, 177,000 new jobs were added (mostly in the private sector), and unemployment held at 4.2%.

- Inflation, according to the U.S. Labor Department (May 13, 2025), while still elevated, has been cooling—especially in sectors such as housing and oil. (The annual inflation rate was 2.3% for the 12 months ending in April, compared to the previous rate of 2.4%.)

- Yes, according to the U.S. Department of Commerce, GDP dipped slightly in Q1 (-0.3%), but the decline was largely driven by companies racing to import goods ahead of potential tariffs, coupled with a slowdown in government spending. Consumer spending moderated – particularly on big-ticket discretionary services like travel and lodging – but overall, consumers remained resilient. (Like me, they were likely also busy stocking up on Amazon orders before prices had a chance to rise.)

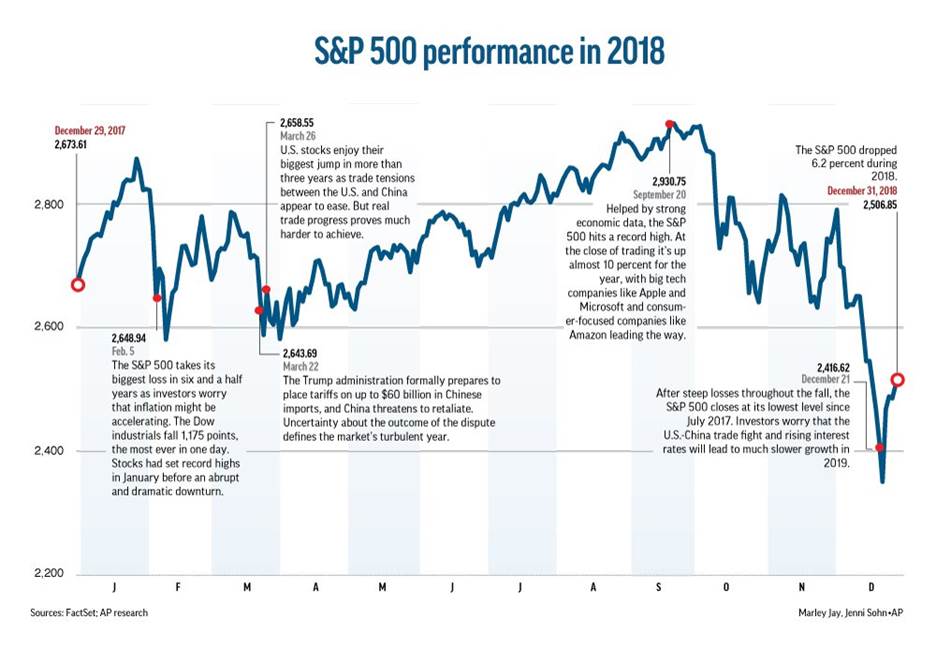

If this all feels a little bit familiar, it should. We saw a similar pattern in 2018, when tariff announcements initially caused a sharp market drop, which was followed by a quick recovery, and then another dip when the real economic impact started to show up in earnings.

It was a classic double-dip market. But, more importantly, it was a great reminder that the second act often brings the real story.

Right now, we’re in that “in-between zone,” again, waiting for the data to catch up to the drama. It’s important to note that the current 90-day tariff pause expires July 9th, and while some effects may trickle in beforehand, the full economic picture—consumer spending, corporate earnings, and inflation—will likely take a few more months to reveal itself.

As the brilliant Cameron Dawson, the Chief Investment Officer of our partner company, NewEdge Capital Group, succinctly said way back in January: “This year is going to be choppy.”

And so far? Cameron has unsurprisingly been right on the money.

Why We’re Neutral—and What That Really Means

Right now, we’re taking a neutral approach to our portfolio strategy. But that is most certainly not because we’re undecided. It’s because we’re being deliberate. Think of it like driving on a drizzly day: You’ve got places to be, so you’re not pulling over. But you’re hopefully not speeding, either. You’re just being a little more cautious than usual, and you’re ready to respond to whatever comes next.

We embraced this approach shortly after the November 2024 election, balancing optimism around pro-U.S. policy with some carefully considered caution. As a flyover (specifically in our active portfolios), that meant increasing exposure to U.S. tech, while also adding gold and other alternative assets to act as shock absorbers in a noisy environment.

In March of this year, also specifically in our active portfolios, my ProsperPlan Wealth co-founder, Chris Grellas, CFP, MSFA, and I diversified even further, mixing growth-oriented stocks with steady, dividend-paying companies. Why would we do that? Because tariffs can increase costs and put pressure on margins. Simply, a “margin” tells you how much money a business keeps from each dollar it earns after covering its costs. If margins start to fall, then stock prices will, too. However, dividend-paying companies not only still send you income quarterly – they also tend to be less volatile in bumpy markets. (Basically – to borrow from our old storyteller friend Aesop – these tweaks represent the tortoise to growth stocks’ hare. And right now, we’re happy to have both in the race.)

Of course, that’s not all we’ve done. We also increased our active portfolios’ international exposure prior to the recent sell-off. Countries like Japan, Mexico, and India, and practically all of Europe, have shown stronger fundamentals and more favorable valuations lately (plus they’ve been less exposed to the recent tariff crossfire). These international positions have already helped cushion the blow during the April sell-off when money rotated out of U.S. stocks and into global markets.

Why We’re Not Going All-In or All-Out

This is where some nuance is helpful. And because your ProsperPlan team loves history – we’re including a comparison to the 2018 tariff market to give you context.

Here’s our approach: If we swing too far into a defensive posture too early – and then the economy holds up or trade tensions ease – we risk missing out on market gains. (And yes, we’ve already seen a near-total rebound from April’s lows.)

But if we lean too hard into risk – and then tariffs hit corporate profits or consumer confidence dips – we open the door to otherwise avoidable losses.

Both the federal reserve and our investment management team know all the above because we’ve navigated a similar tariff situation in the recent past. In late 2018, the markets not only bounced back from early tariff-related fears – but had fully recovered by September – only to stumble again when rising costs and inflation began showing up in the actual data. By April of 2019, however, the market had not only recovered but had surged to new highs. That double-dip market once again proved a valuable lesson: stay flexible, stay patient, and don’t overreact to the first plot twist.

What We’re Watching Next

To get even more granular, our team is closely analyzing three key areas as we move into the second half of 2025:

- Employment & Inflation Data – The upcoming jobs reports and inflation readings will offer insight into whether tariffs are starting to affect hiring or consumer prices.

- Corporate Earnings Guidance – Q1 earnings were strong, but companies are extremely cautious. We’re watching for signs of margin pressure (increased expenses eating into corporate earnings), especially in global manufacturing and import-heavy sectors.

- Global Market Trends – The shift in global supply chains is undeniably accelerating. And that means that Europe, India, Mexico, and Japan are worth watching—not just as economic partners, but as investment opportunities.

Sure, as one of our readers astutely pointed out, the road ahead could lead to inflation, recession, stagflation, or… it could all just be more of the same. At this moment, these scenarios are still unwinding, and we’ve calculated that we are only just about 40% of the way through this cycle. The rest of the plot will be written as fresh economic data rolls in, especially after July 9th, when the current tariff pause expires.

But one thing we know for sure is that stock values rise and stock values fall based on earnings. And with tariffs still in negotiation, no one and nothing – markets included – can confidently predict the impact on earnings, profits, or stock values just yet.

In the graphic below, we’ve outlined three potential market paths based on statistical models – and yes, they’re a bit like those “choose your own adventure” books, but the difference is that these are based on statistics and long-term economic data.

In the best-case scenario, if corporate earnings reports come in stronger than expected, we could potentially see markets climb 8 to 12%. That kind of optimism would probably cause investors to ditch bonds in favor of stocks, sending the 10-year Treasury yield higher as everyone chases returns. (This would not at all be great for the mortgage market.)

On the flip side, if we enter an earnings contraction – where company profits start to slide – we could be looking at a classic double-dip downturn. (Think of it as the market equivalent of stumbling, getting back up in a rush, and then tripping on your shoelaces all over again.)

How ProsperPlan Portfolios Are Currently Positioned

As always, we manage with purpose, patience, and a plan. That’s at the foundation of everything we do. Remember:

- We are very well diversified. The U.S. remains an innovation powerhouse, but we’re also expanding our reach to benefit from momentum in international markets and to reduce overexposure to any one region.

- When and where needed, we include “inflation-aware” assets. Our portfolios may hold TIPS, gold, or real assets designed to help preserve purchasing power if inflation creeps back in.

- We maintain savvy bond exposure. Bonds may not be exciting, but they’re dependable. For most clients, we recommend holding at least three years of income in bonds to provide stability, income, and flexibility from which to take distributions in down markets. Many of our clients hold between 15% and 50% of their portfolios in bonds, though this varies based on individual goals and risk tolerances.

- We prioritize high quality companies. Whether it’s U.S. growth stocks, dividend-paying blue chips, or international value stocks, we focus on companies with good cash flow, strong balance sheets, and the ability to weather uncertainty without skipping a beat.

- We work with a world-class team. Through our collaboration with NewEdge, we’re supported by some of the best minds in the industry. This includes direct access to BlackRock’s global research and investment strategy teams. That means we’re not just reading headlines—we’re plugged into the deeper analysis behind them.

Final Thoughts

A quick shoutout to the client that sparked this conversation: Thank you! Your experience, perspective, and healthy skepticism are exactly the kind of mindset we appreciate. You’ve seen what markets can do—and you understand that “staying the course” doesn’t mean standing still.

At ProsperPlan, our goal is always the same: To help you grow and protect your wealth through thoughtful, proactive planning. That’s why we’re watching the signals, analyzing the data, and staying ready to act with clarity and confidence.